Sustaining a business requires not only generating revenue but also managing cash flow effectively to ensure liquidity and operational stability. Cash flow represents the movement of money in and out of the business, impacting short-term obligations and long-term growth. Managers must closely monitor how cash inflows from sales, investments, and financing compared to outflows, such as expenses, loan repayments, and dividends. A clear understanding of cash flow dynamics allows decision-makers to anticipate financial challenges, optimize working capital, and allocate resources strategically. Whether adjusting inventory levels, renegotiating credit terms, or evaluating investment opportunities, sound cash flow management is essential for maintaining business viability and driving sustainable growth.

There are many decisions taken in the business operations, which can be broadly classified into three categories:

- Financial decisions > Pertaining to the acquisition and management of equity, debt

- Investment decisions > Focused on asset allocation, capital project expenditures

- Operational decisions > Related to day-to-day business functions, cost management

Each of these decisions influences the company’s net cash flow, either through inflows or outflows, thereby affecting the financial sustainability and growth potential of the organization

The primary source of income for any business is revenue from operations. However, various expenditures and cash outflows reduce the available funds, consequently limiting reinvestment opportunities and business expansion

The budding managers when analyzing the cash flow statements, must answer the key questions to assess the financial performance and making the decisions for the following year, the focus must vary based on the position, the vertical heads, the CEO, the board etc..

Key observations and question that managers must address from cash flow statements before making decisions for the next year

1. Evaluating Cash Flow Sufficiency for Expansion & Payments

Do we have enough internally sourced cash flows to meet expansion needs, or do we need external funds?

Strong internal cash flows help avoid interest costs and ownership dilution, while external funds accelerate growth and provide strategic partnerships.

2. Identifying Major Sources of Cash Inflows

Review cash inflows from operational, investing, and financing activities.

If core operating activities generate most cash, it signals strong business fundamentals and sustainable growth.

3. Strategic Use of Net Cash at Year-End

Cash should be allocated toward future growth and business expansion investing in new plants, production lines, or geographic expansion. Such investments must align with long-term business vision & strategy.

Good Uses of Cash:

- Reinvest in growth: Capacity expansion, R&D, talent development, modernization.

- Strengthen financial position: Repay loans, improve working capital.

- Optimize investments & shareholder value: Dividends, M&As, stock buybacks.

Risks & Misuse of Cash:

- Poor investment decisions, especially if linked to board members or promoters.

- Financial mismanagement, lavish executive payouts, excessive dividend distribution, deviation from core strategy.

4. Assessing Net Cash Flow Sufficiency for Investments & Obligations

Financially healthy companies internally source funds for expansion and payments (rents, interest, dividends).

Net cash flow should primarily come from operational activities, not from investment or financing, which are supplementary. If external sources continuously exceed operational cash flows, the business may be deviating from its core purpose. Prioritize investments over aggressive repayment of low-interest loans, as excessive debt reduction may limit growth.

5. Investing in Assets vs. Depreciation

Fixed assets (machinery, buildings) depreciate annually, losing value over time. Investments in new assets must exceed depreciation to sustain operations and drive expansion.

6. Monitoring Borrowing Trends

Evaluate whether long-term and short-term borrowings are rising continuously—if so, it’s a cautionary sign.

7. Analyzing Working Capital Changes

Working capital involves accounts receivable, accounts payable, and inventory. Longer payable terms and shorter receivable cycles indicate good financial management, allowing operations to run on leveraged funds. Minimize inventory holding days to optimize cash flow.

8. Measuring Interest Coverage

The interest coverage ratio compares interest obligations to net cash inflow from operations. A higher ratio indicates strong cash generation to meet obligations.

9. Evaluating Cash Flow Trends

Trends in operational & investing activities should be moving upward, signalling sustainability and growth. Financing activity trends depend on decisions—equity issuance increases cash inflow, while debt repayment lowers cash flow.

Financial decisions

Financial decisions play a crucial role in shaping the company’s financial structure, bringing in equity, retained earnings, and debt financing. These decisions also lead to cash outflows in the form of interest costs, dividend distributions, principal repayments, and other obligations

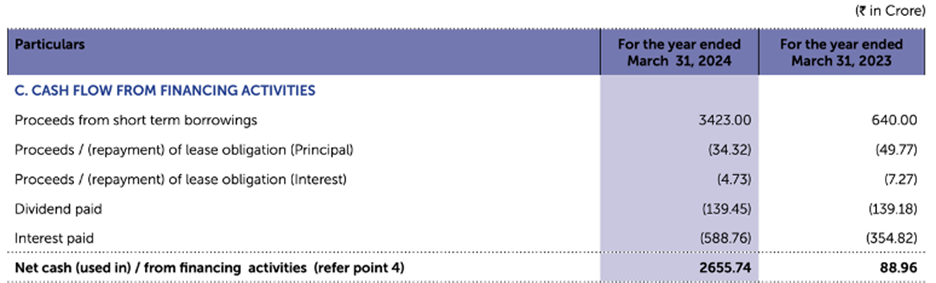

Operations in cash flow statement from financing activities:

- Added > Cash raised from selling shared

- Added > Borrowed money

- Deducted > Buy back of shares

- Deducted > Repayment of Loans

- Deducted > Dividend payments

- Deducted > Lease obligations

See below illustration from BHEL annual reports for the FY 2023-24:

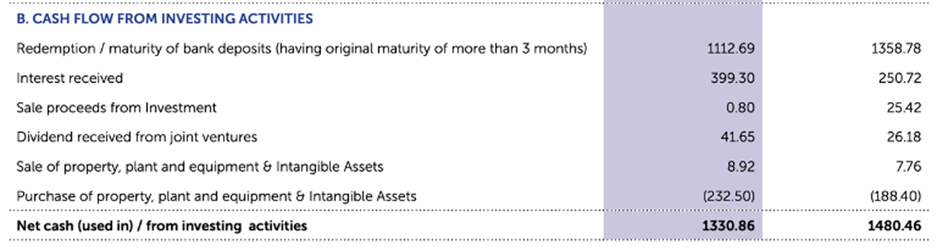

Investment decisions

Investment decisions are taken to acquire new assets such as plant equipment, buildings, technology or for expanding the production capacity or for research and development. There can be decisions for investing in subsidiaries, M&As, or investments in financial instruments. While the financial investments bring cash into the business, the other investment decisions will result in cashflows from the business.

Operations in cashflow statement from investment activities:

- Added > Sales of PPE, Interest received, Dividend received etc.

- Deducted > Purchase of PPE

See below illustration from BHEL annual reports for the FY 2023-24:

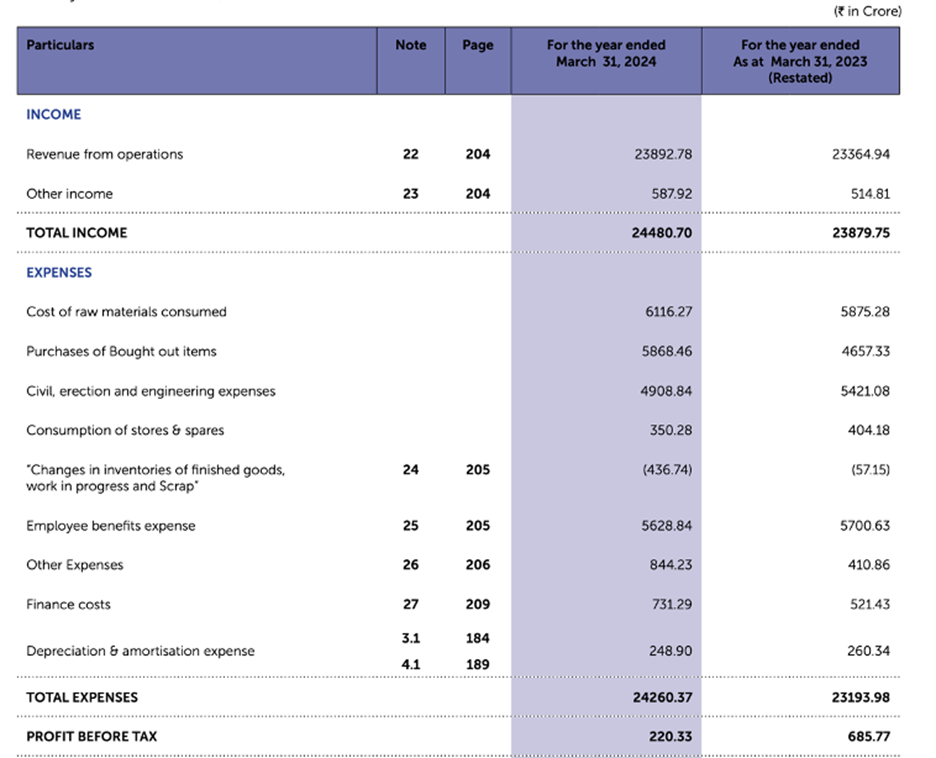

Operational decisions

There are many operational decisions taken across functions like production planning, material mgmt., product quality control, production optimization, product supply chain and logistics.

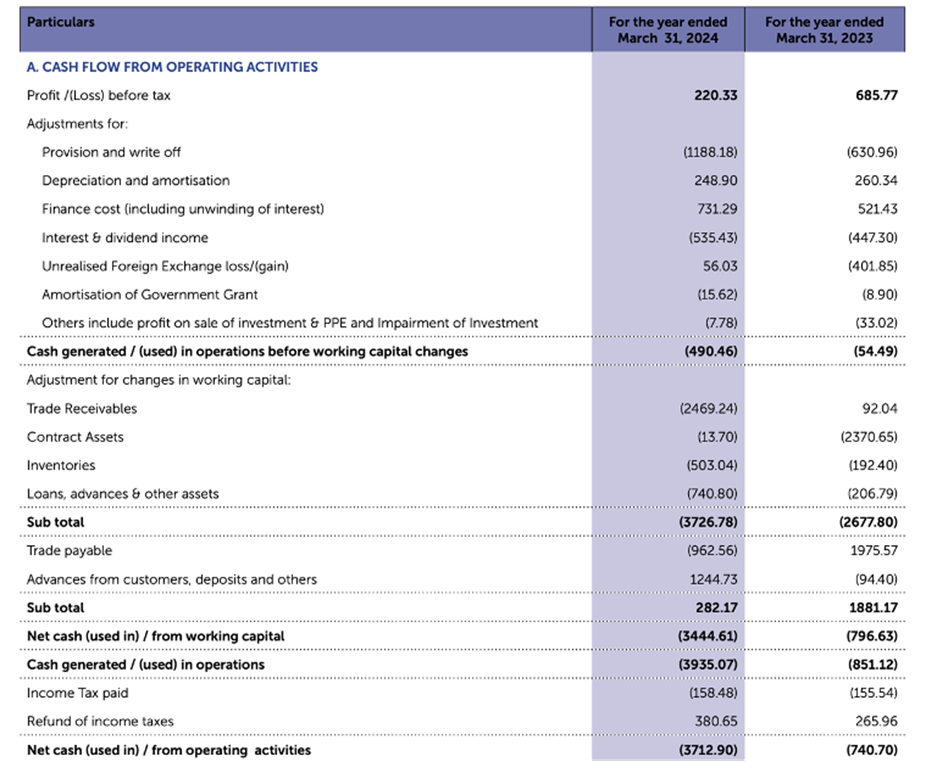

Operations in cash flow statement from operational activities:

- Added > Net income, taken from Income statements, which is a starting point

- Added > Depreciation & Amortization, since they are non-cash expenses

- Changes in Working Capital (Inventory, Accounts Receivable, Accounts Payable)

- Added > If decrease in Accounts Receivables, cash collected from sales

- Added > If decrease in Inventory, as inventory sold and cash received

- Added > If increase in Accounts Payable, expenses incurred but not yet paid

- Deducted > If increase in Accounts Receivables, sales made but cash not received

- Deducted > If increase in Inventory, cash spent on stock

- Deducted > If decrease in Accounts Payable, cash used to make payments

See below illustration from BHEL annual reports for the FY 2023-24:

The below table summarizes the net cash to the business for BHEL

- Net cash from financial activities: 2655.74 Cr

- Net cash from Investment activities: 1330.86 Cr

- Net cash from Operational activities: -3712.90 Cr

Net cash addition to the business in the Financial Year: 273.70 Cr

Conclusion

Without a steady flow of cash and proper management of this cashflow, even the most profitable businesses can struggle to meet their commitments and sustain growth. Managing cash flows effectively ensures not only day-to-day stability but also long-term resilience, enabling businesses to invest and expand. A strong cash flow foundation is key to financial health and strategic decision making, allowing organizations to honor their obligations while seizing new opportunities.

References

1. “Accounting Simplified” book by Prof. Rachappa Shette, IIM Kozhikode

2. BHEL Annual Statements accessed from https://www.bhel.com/annual-reports