EXECUTIVE SUMMARY

Satyam Computer Services was once India’s fourth largest IT company, trusted by global clients and investors alike. In January 2009, founder B. Ramalinga Raju confessed to orchestrating a decade long accounting fraud worth over 7,000 crore, exposing catastrophic failures in corporate governance, auditing, and board oversight. This case remains one of the most studied examples of financial fraud in Indian corporate history.

1. Background

Founded in 1987 by B. Ramalinga Raju, Satyam Computer Services grew into a global IT powerhouse with over 50,000 employees operating across 60+ countries. By 2007–08, the company reported revenues of ₹8,394 crore and was considered a peer of Infosys, Wipro, and Tata Consultancy Services. Investors, analysts, and global clients placed enormous trust in the company’s financial health.

2. The Fraud: What Actually Happened

On January 7, 2009, Ramalinga Raju submitted a letter to the Board of Directors confessing that Satyam’s financial statements had been falsified for years. The total misrepresentation stood at approximately ₹7,136 crore, making it one of the largest accounting frauds in Indian history.

Breakdown of Falsified Figures

| Fraudulent Item | Amount |

| Non existent cash & bank balances | ₹5,040 crore |

| Accrued interest that never existed | ₹376 crore |

| Understated liabilities | ₹1,230 crore |

| Overstated debtors (receivables) | ₹490 crore |

| Total Misrepresentation | ₹7,136 crore (approx.) |

Quarterly Profit Manipulation (Q2 FY2008–09)

| Item | Reported | Actual |

| Revenue | ₹2,700 crore | ₹2,112 crore |

| Operating Profit | ₹649 crore | ₹61 crore |

| Operating Margin | 24% | ~3% |

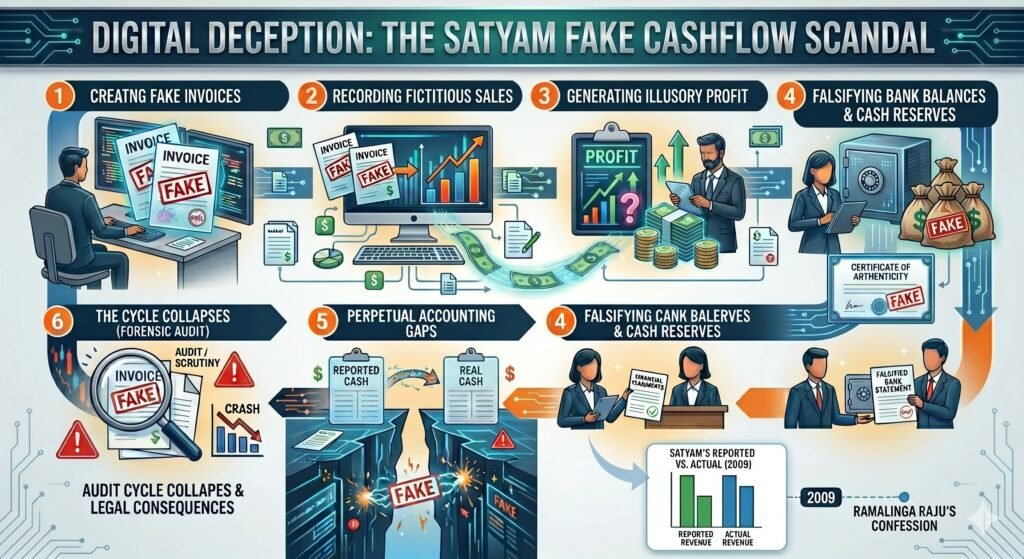

The company was inflating profits by nearly 10 times their actual value. Fake sales invoices, investigators later found evidence of nearly 7,000 fabricated invoices were entered into Oracle Financials to artificially boost revenues. Since fake revenues created fake receivables, management then forged bank statements and fixed deposit receipts to show the supposed “collection” of these amounts, creating a fiction of over ₹5,000 crore in cash.

3. How the Fraud Operated

The mechanics relied on three interlocking deceptions:

- Fake invoices inflated revenue and receivables in the ERP system.

- Forged bank statements converted fake receivables into fake cash, hiding the revenue cycle.

- Ghost employees (≈10,000 suspected) enabled salary based siphoning of real funds.

Importantly, no single system was “designed for fraud”, management simply overrode internal controls, exploited weak password policies, and provided auditors with fabricated documentation rather than allowing independent bank confirmations. Raju himself described the situation as “riding a tiger without knowing how to get off”, each quarter requiring larger fabrications to meet rising market expectations.

4. The Trigger: The Maytas Acquisition

By late 2008, the fraud had grown unsustainable. The books showed over ₹5,000 crore in cash that did not exist. In December 2008, Satyam announced a plan to acquire two family linked companies, Maytas Infra and Maytas Properties for approximately $1.6 billion (₹7,800 crore). Analysts believe this was an attempt to replace fictitious cash on the balance sheet with real physical assets.

Shareholders immediately revolted. The stock fell 55% in a single day. The deal was cancelled within hours. Weeks later, under mounting pressure, Raju confessed in writing to the fraud.

5. Corporate Governance Failures

Board of Directors

The board failed to challenge management on related party transactions, question the implausibly high cash balances, or exercise independent judgment. The Maytas deal clearly a conflict of interest, was initially approved without adequate scrutiny.

Auditor Failure (PwC)

PricewaterhouseCoopers served as Satyam’s statutory auditor throughout the fraud. The central failure was reliance on management provided evidence rather than direct, independent bank confirmations. PwC faced regulatory penalties in India and abroad and the case became a global benchmark in audit accountability.

Weak Internal Controls

Internal systems lacked effective segregation of duties, access controls were insufficient, and there was no independent mechanism to flag discrepancies between reported cash positions and actual bank records. Governance existed on paper; enforcement did not.

6. Impact

| Area | Impact |

| Investors | Share price collapsed from ₹500+ to under ₹20. Thousands of crores in wealth wiped out. |

| Employees | 50,000+ jobs placed in uncertainty; salary concerns widespread. |

| India’s IT Reputation | International concerns raised about accounting quality and governance standards. |

| Auditing Profession | Global scrutiny of PwC; questions about audit independence across the industry. |

7. Resolution & Recovery

The Indian government acted swiftly: the existing board was dissolved and new government appointed directors stabilized operations. In April 2009, Tech Mahindra acquired a 31% controlling stake at ₹58 per share (₹2,900 crore deal value), rescuing the company. Rebranded Mahindra Satyam, it eventually merged fully into Tech Mahindra and is considered one of India’s landmark corporate rescue stories.

In 2015, Ramalinga Raju and several associates were convicted on charges of criminal conspiracy, cheating, forgery, and breach of trust.

8. Key Lessons

| Lesson | Implication |

| Profit without cash flow is a red flag | Strong reported profits alongside weak operating cash flows demand scrutiny. |

| Independent boards are not optional | Directors must actively challenge management, especially on related party deals. |

| Audits require independent verification | Relying on management provided evidence is insufficient; direct bank confirmations are essential. |

| ERP systems are not fraud proof | Software is only as trustworthy as the controls and people around it. |

| Scale amplifies consequences | Fraud that starts small compounds rapidly when external expectations keep rising. |

| Ethics underpin all governance | Reputation built over decades can collapse within days. |

9. Regulatory Reforms Post-Satyam

The scandal directly shaped India’s corporate governance framework, with lasting reforms embedded into the Companies Act 2013 and SEBI regulations:

- Mandatory rotation of statutory auditors to prevent complacency.

- Strengthened requirements for independent directors on boards.

- Tighter disclosure norms for related party transactions.

- Enhanced accountability for audit firms, including NFRA (National Financial Reporting Authority) establishment.

- Whistleblower protection provisions strengthened.